Current State of Inflation

Inflation is a topic not only making headlines but also one that you have likely been seeing at the grocery store, the gas pump, and on almost all your regular purchases. Inflationary pressures began as we started to recovery from the economic shock of the pandemic. Many U.S. consumers had increased their savings rate during the pandemic and accumulated excess cash. This additional savings combined with the fact that Americans could not easily spend money on the goods and services they desired during the pandemic created a heightened demand as restrictions started to ease. In addition to increased demand many suppliers had reduced production during the pandemic and could not keep up with demand as things returned to normal. This was exaggerated by the large hold ups in the supply chain. All of this created a recipe for inflation.

Today we have two more forces affecting the outlook for inflation – wage inflation and the price of commodities. We are currently back to a historically low unemployment rate and in many sectors of the economy we have more available jobs than job seekers. This need to keep a strong work force when a job seeker has so much power pushes wages upwards. This portion of inflation can be more widespread and stickier. Labor is needed in the production of almost every good and service and therefore affects the price of most goods and services. Moreover, it is very difficult to reduce wages once they have been increased. The price of commodities is another major factor for inflation. There are several factors affecting this, however, the tragic war in Ukraine has been a large contributor. This is because Russia is the third largest producer of oil and a major producer of potash which is used as fertilizer. Increases in oil prices not only affect the price you pay at the pump but also the cost of transporting goods. Increased cost of fertilizer is likely to be reflected in increases in the cost of food.

Currently (as of April 1, 2022) the inflation rate is anywhere from roughly 5% to over 7% depending on the index you look at. It is important to keep in mind that some amount of inflation is good as it indicates that economy is growing. The Federal Reserve has historically targeted an inflation rate of 2%. During their March meetings they have indicated they will be increasing interest rates in effort to combat inflation but will be data dependent on future interest rate hikes.

Why Inflation Matters to Your Financial Plan

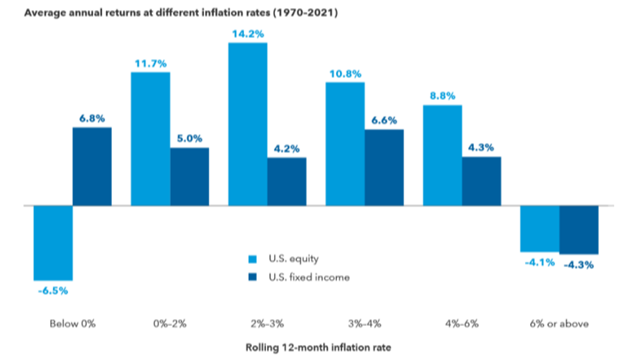

So, what does this all mean for you portfolio and how might this affect my financial plan? History gives us some indication what inflation might mean for your portfolio. The chart below shows historical returns of the stock and bond market during various inflationary periods. During periods of modest inflation both the stock and bond market have historically performed well however during periods of disinflation or extreme inflation both come under pressure.

Sources: Capital Group, Bloomberg Index Services Ltd., Morningstar, Standard & Poor’s. As of 10/31/21. All returns are inflation-adjusted real returns. U.S. equity returns represented by the Standard & Poor’s 500Composite Index. U.S. fixed income represented by Ibbotson Associates SBBI U.S. Intermediate-Term Government

Bond Index from 1/1/70–12/31/75, and Bloomberg U.S. Aggregate Bond Index from 1/1/76–10/31/21. Inflation rates are defined by the rolling 12-month returns of the Ibbotson Associates SBBI U.S. Inflation Index.

We believe that is important to keep a long-term perspective when considering inflation and your portfolio. Historically periods of high inflation have not lasted forever. Higher inflation typically leads to lower demand for goods and services which naturally lead to lower inflation. Moreover, actions taken by the Federal Reserve can work to combat high levels of inflation. With all this being said it is very difficult to predict how long inflation will stay elevated. It seems likely that inflation will stay elevated for some time. If inflation stays elevated, it will require investors to seek out higher returns to keep up with the increased cost of living.

Younger investors who are still working should have less concern about inflation. Their longer time horizon before assets are needed mean they have the ability to take on greater risk in their portfolio. Moreover, they have the ability to demand wage increases to keep up with inflation. Investors in retirement are at greater risk because they can not rely on wage increases and often do not have the ability to take on substantially greater risk in their portfolio. Retirees with large cash savings who rely heavily on fixed income sources without cost-of-living adjustments are at the greatest risk. Wherever you are at in life and whatever your situation there are steps you can take to help prepare yourself and your portfolio for periods of higher inflation.

Contact Us

What You Can Do

Stay Invested

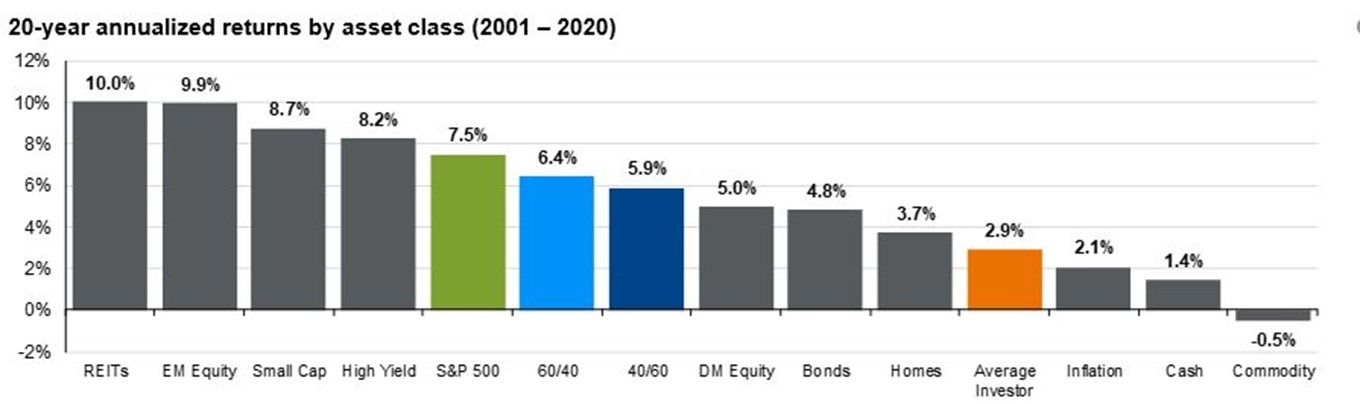

Periods of inflation can often come with uncertainty and market volatility which makes staying invested more difficult. However, staying invested becomes very important in times of inflation. Those with large cash balances will start to see their purchasing power quickly eroded. Both stocks and bonds on the other hand have outperformed inflation over the long run. Given this we suggest growing savings instead of cash during periods of inflation. This comes with the exception of those who need their assets to meet short-term expenses. The chart below shows historically returns of various asset classes for the last 20 years. From the chart you can see that over a long time horizon both stocks and bonds outperform inflation while cash savings struggle to keep pace.

Source: Bloomberg, FactSet, Standard & Poor’s, J.P. Morgan Asset Management; (Bottom) Dalbar Inc, MSCI, NAREIT, Russell. Indices used are as follows: REITs: NAREIT Equity REIT Index, Small Cap: Russell 2000, EM Equity: MSCI EM, DM Equity: MSCI EAFE, Commodity: Bloomberg Commodity Index, High Yield:

Bloomberg Global HY Index, Bonds: Bloomberg U.S. Aggregate Index, Homes: median sale price of existing single-family homes, Cash: Bloomberg 1-3m Treasury, Inflation: CPI. 60/40: A balanced portfolio with 60% invested in S&P 500 Index and 40% invested in high-quality U.S. fixed income, represented by the Bloomberg

U.S. Aggregate Index. The portfolio is rebalanced annually. Average asset allocation investor return is based on an analysis by Dalbar Inc., which utilizes the net of aggregate mutual fund sales, redemptions and exchanges each month as a measure of investor behavior.

Guide to the Markets – U.S. Data are as of March 31, 2022.

The Role of Stocks

Stocks play a vital role in helping investors produce returns that keep up with inflation. Although stocks are not an inflation hedge, they tend to do much better than inflation over longer periods of time. It is our belief that having a well-diversified stock portfolio is important during these periods of time. We also believe that choosing your stock investments wisely is important. We often see larger disparities in the winners and losers during periods of rising inflation. Those companies that have the potential to do better are high quality companies that have the ability to increase prices with highly demanded goods and services. Your portfolio should have a tilt towards these high-quality companies.

The Role of Bonds

Bonds, although likely to come under pressure as the federal reserve increases interest rates, still have an important role in a portfolio. Bonds can provide a role as a diversifier and a modest return. We believe it is also important to stay diversified when considering bonds as a part of your portfolio. Some fixed income investments such as floating rate loans or Treasury Inflation Protected Securities (TIPS) have the ability to increase the interest rate they pay investors during periods of rising inflation. Incorporating some high yield bonds can help insulate your bond portfolio against the risk of rising interest rates. Also, consider short term bonds as they are less sensitive to increases in interest rates than longer dated bonds.

Consider Other Asset Classes

In addition to stocks and bonds, we believe it is important to consider other asset classes. Real estate has historically been a good hedge against inflation. This is because real estate has a unique combination of increasing income, appreciating value, and depreciating debt that helps it keep up with rising costs. An investment in real estate can be made in many ways such as buying a rental property or investing in a real estate investment trust (REIT). A tradable REIT or mutual fund that invests in REIT would be appropriate for most investments looking for diversification and professional management of your real estate investment while maintaining liquidity.

Investors might also consider hedged strategies. These mutual funds and ETFs allow investors to hedge some of the downside risk of investing in the stock market while incrementally participating in the upside. This is done using direct investment in the stock market combined with the use of derivatives. These types of strategies can be helpful in an environment where more equity like exposure is needed to produce higher returns. They can be used as a way to potentially take on less risk than stocks and produce higher returns than bonds.

The final category often considered in inflationary periods is commodities. Periods of inflation are often largely driven by increases in commodities and as such investments in commodities tend to do very well in these time periods. The caveat with commodities is that they tend to be very volatility, speculative and have not historically produced strong returns for investors. For this reason, many investors poorly time their investment in commodities and misuse them in their portfolio.

Watch Your Wallet

In addition to changes made to your portfolio individuals should be aware of their spending habits and consider negotiating those things that are negotiable. An awareness of your spending habits can be helpful to alter your spending if needed. This doesn’t mean you need to be tracking every penny you spend but rather having a general awareness will help you make better decisions about your spending. One of the easiest ways to do this is by using a monthly spending tracker. Most credit cards allow for some tracking and categorization of your spending and there are many resources online for this. Individuals should also consider negotiating those things that are negotiable. This might include your salary or your rent payment. Most things you buy are not negotiable but a win in a few big categories such as your salary and rent can make a big difference in your financial picture.

Work With an Accredited Advisor

Working with an accredited advisory team that has successfully navigated market events in the past can be important in helping navigate times of uncertainty. A good advisor will take the time to understand your specific situation and tailor a set of solutions for you. This advisor can also be helpful in seeing the big picture and bringing specialized knowledge to your situation. Many people find great peace of mind by working with an advisor and have the potential for an improved financial situation.

If you are considering working with an advisor or want to know if you are taking the right steps to prepare for inflation, please give us a call.